Carrier – Principal

Agents - Are you looking to get a quote for a group?

Principal Life Insurance Company, a member company of the Principal Financial Group® (The Principal®), offers a wide variety of employer- and employee-paid insurance solutions to create a custom benefits package for any business, no matter what size—including easy administration and excellent service to give you an edge.

Interested in other Carrier Product Update Videos? See all videos here.

Jason Powers:

It is time for another carrier product update. Tune in as we talk directly to the carriers about their new plans, any new network options they have, or which plan designs offer the most savings and learn about the tools and resources they offer to help you generate more business. Visit our website to learn about all of the carriers we quote in our carrier product update series.

Jason Powers:

Hello and welcome back to our carrier product update series. [00:00:30] Today I’m joined by Greg Kane, a sales executive of group Benefits division at Principal Financial Group. Welcome back, Greg.

Greg Cain:

Thank you. I appreciate it. I’m glad to be back.

Jason Powers:

Yeah, I heard you got a lot of accolades this last recording, so it’s time to update everybody on what’s going on in principal.

Greg Cain:

Yes sir. A lot of shout outs last year.

Jason Powers:

Yeah, well good stuff. Well, we want to make sure that we arm you the broker with as much information as possible as you go out and prospect for new clients. And so we’ll get started. [00:01:00] If for a broker that’s never sold principal, what’s the important thing that they need to know about Principal as a company and your position in the market?

Greg Cain:

Yeah, I think that’s a great question. And I mean Principal Financial Group and principal Life we’re a traditional ancillary carrier, a non-medical space focusing on life insurance, disability, dental, vision. And then recently in the last few years we’ve kind of expanded our portfolio [00:01:30] and include work side benefits, hospital indemnity, critical illness and accident coverage. And so that’s kind of the product suite, but I think we’re built on small employers being strong partners to our broker community being easy to work with

Jason Powers:

For sure. I know at least in our experience and my experience as a broker before Legacy, but over the last 10 years as a general agent working with principal, I know our team really does feel that it’s a partnership [00:02:00] amongst our two companies, and we certainly see the support that you give as a carrier in the marketplace and then the products that you have in your portfolio, I think fill the void for a lot of these groups that are trying to give a good employee benefit package to their employees to help them recruit, retain, or reinforce their culture.

Greg Cain:

Right. Yeah, I would say, I mean, look, we’re more than obviously just products and the history. I mean, it really comes down to people and I think we are people and [00:02:30] people company mean we really value our personal relationships within the office. Of course, it extends out to our broker partners, and that’s probably the one thing that I think differentiates us the most is that local sales and support team, our focus really two lives and up. It’s essentially that same sales and support team any case size, but our bread and butter really is that small case a small employer fit.

Jason Powers:

Well, let’s get into the product portfolio. So these are the lines you offer, the different [00:03:00] size groups, different segments I would say, right?

Greg Cain:

Yeah. So we talked earlier, I mean I kind of briefly went over the laundry list of benefits we work with. Obviously it’s here on the slideshow as well. We do start at two lives, so two employees up. I mean really there is no ceiling, although it does say here, 5,000 enrolled lives. I’d say if we’re going to get large case go above headquarters, what we would say is our sweet spot, which is again, small employers under 200 [00:03:30] lives. I think we’re progressively better as we get smaller, but if we go above that threshold, I think we’re comfortable playing with and we have success earning business up to that 5,000 life threshold. Above that, we’re really not built to write the Jimbo cases, but if you look here, two lives in out for employer paid, we can do voluntary coverages across the board, but we do need at least five eligible to play in the voluntary space. That’s a pretty low threshold. [00:04:00] A lot of our competition does draw the line of the sand a little bigger than that. Now that’s five eligible. We only need two enrolled, so five eligible to quote it, two enrolled it to write it, and then of course the compliment What we do in that larger case arena, we do offer some self-funded solutions on dental, short-term disability and vision insurance.

Jason Powers:

Sure, that makes sense. And I think the core benefits, the dental, the vision, the life, maybe even the disability [00:04:30] I think probably are the core benefits that we see a lot. But something that you’ve been talking to me about for a long time, and my good friend Rob had been trying to get me on board with some of these things before. If we go back in time, back in the way back machine is supplemental benefits. And these are things that I know as a broker, I didn’t really spend a whole lot of time really marketing, but as a general agent and working with agents out in the market, these are products that can really fill a need, [00:05:00] particularly for the kind of plan designs we see on the medical side.

Greg Cain:

Right. Yeah, I think when we talk about what’s new at principle, I think this is new, our most recent additions to our portfolio have been these types of products. Critical illness was rolled out for us seven or eight years ago. Accidents followed quickly after we just introduced hospital indemnity in the last six months or so, and in the Midwest were licensed, were filed and approved in every state. There are some pockets out [00:05:30] there that we’re still working through the filing process, but these are products that are new to us, but not so much challenges for us. That place, I would say one out of every three groups I sell have one of these products attached to it. And it goes to the point you just made. I mean a lot of employees from an employment of a package, there’s some risk, there’s some financial exposure there from the medical plan, the high deductible plans kind of deliver that obvious potential risk from an employee perspective on out-of-pocket expenses. [00:06:00] And these products are built to help contain that a little bit.

Jason Powers:

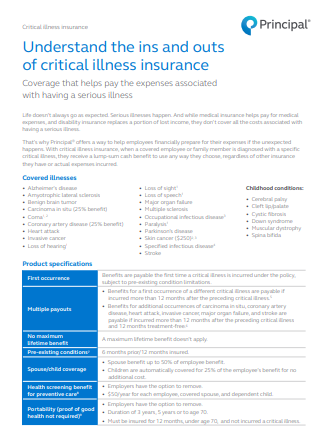

Well, let’s dive into one. So critical illness I think was the first one that you have here. When I think of critical illness, I think of some of the commercials I see on TV for certain products, but it’s more than that, right? We’re not talking about cancer only or one specific medical condition. This has kind of a broad spectrum of conditions that it [00:06:30] covers,

Greg Cain:

Correct? Yeah, this is pretty long. But yeah, the big ones are cancer, heart attack, stroke, things like that. Again, it’s built to bridge that financial gap from a health insurance perspective. And it also can do more than that as well. The employee isn’t obligated to use our benefit proceeds to pay just for their deductible. They can use it forever. They want to use it, but the need arises from that health insurance plan design.

Jason Powers:

There’s a lot of financial obligation built into these high deductible [00:07:00] plans where they’ve got, maybe they’re okay with a smaller copay on your day-to-day office visits and prescriptions, but the real scary sticker shock number is the high deductible, high out of pocket maximum. And that’s where this can really bridge that gap.

Greg Cain:

Correct? Yeah. So if you look here, we just kind of mentioned these cancer heart attack. Yeah,

Jason Powers:

Common diseases.

Greg Cain:

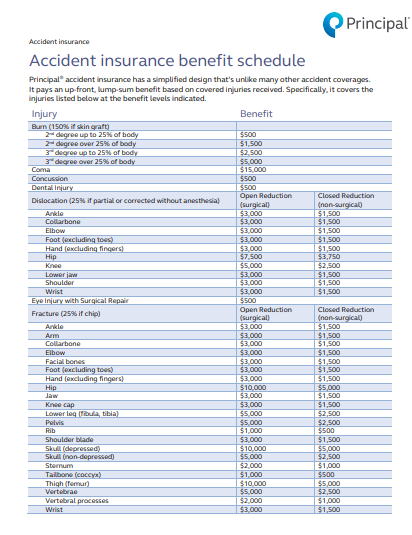

We talk about how [00:07:30] is the plan structured, and so a common question is can something be covered more than once? And the answer is yes. We will pay for the same illness multiple times. We can pay for different illnesses several times. There is a lifetime max within the contract, and so whatever the scheduled benefit is, we’ll pay two times that amount, and once that employee or member hits that two times amount, we will automatically take ’em off the plan and stop billing for them. So obviously they’ll be on the plan and be paying premium [00:08:00] up until the situation where they do maximize the benefit, but it’s really how often does it happen? Probably not often, but it could. And if it does, we’ll take them off. And that’s a standard provision and most critical illness contracts.

Jason Powers:

Got it. So then let’s see, next slide here. So then more of the covered critical illnesses we have here. Walk me through this slide here. I looked at this one, and this is where I get [00:08:30] outside my comfort zone being the guy that sells a lot of medical.

Greg Cain:

So this, we’re really get into the details of the product. I mean the critical illness, unlike disability insurance where there’s a lot of variables, we can really dig into a lot of the facets of that contract. It’s kind of black and white, it kind of is what it is. And these are kind of the listed illnesses that are covered and how the plan’s going to pay. So if you look at those top two on the left hand side, carcinoma insight two, coronary artery disease, [00:09:00] we’re going to limit the benefit to 25% of what the employee elected. So if the employee elected $10,000 of coverage through a critical illness offering, then if those claims were submitted, we’d only pay 2,500 a common in the industry, the bottom four, they’re heart attack, invasive cancer, organ failure, stroke, we’re going to pay the full amount elected for those. And of course, we talk about first occurrence only. So again, you go down that list. I mean, skin cancer, we’re going to do one diagnosis of skin cancer, we’re going to pay [00:09:30] two 50 or the first diagnosis of Alzheimer’s disease, we’re going to pay the full benefit. And then of course, we also have child specific illnesses as well.

Jason Powers:

Got it. Valuable benefits for sure. And those are all, I mean, I look at that list of illnesses, those are all scary ones to think about. And someone on a high deductible plan knowing that they’ve got a benefit there to help them cover not only their deductible expenses, but like you mentioned, I mean some of the other, [00:10:00] I’d say ancillary expenses that come along with getting diagnosed with exactly

Greg Cain:

Lot loss of work. So it points to this right here. I mean you talking about what are these benefits really to cater to it is that financial risk and exposure to a major medical event, but it really points to the first bullet there, the medical deductibles and copays. You’ve got loss of income, childcare expenses, travel costs, all this stuff or results of that major medical event [00:10:30] as listed in the prior slide.

Jason Powers:

Alright, so not just critical illness, I guess more key features on critical illness.

Greg Cain:

Yeah, it keeps going. So yeah, again, we’re going to deliver coverage for both the employee and families. I don’t know if this is, I’m not sure how unique this is with principal, but I’ll tell you if the employee elect coverage, the child is covered automatically, no premium. So the employee elects coverage, any eligible child is on the plan regardless of even enrollment, they’re on the plan and [00:11:00] they’re covered under the policy and there’s no premium in that regard. They can also elect spouse coverage coverage, and then there is a wellness

Jason Powers:

Back up there. I think that’s critical to understand. It’s a composite premium for employees and it includes families regardless of whether or not

Greg Cain:

It includes the child premium, it includes the child premium. So there’s going to be, it’s priced a lot like voluntary life. It’s going to be age banded rates. So every five year age band, the rate, the rate will [00:11:30] likely increase. Spouse will have their own rate to rate table similar to the employee rate table. If the employee elects covers and they have eligible children, the child’s covered automatically. Got it. No questions asked.

Jason Powers:

Okay. So then the spouse is separate, it’s a separate premium, but the kids are always covered.

Greg Cain:

Okay. Correct. Yep. The health screening benefit right there, that’s just a wellness exam benefit. We default to $50. There was some flexibility there, but it’s just a way to get some money back from the plan because this is truly is an insurance product. So [00:12:00] unlike dental or vision where you buy those products to use them, you’re buying critical illness in hopes that you never have to use ’em. You might have a family history with some of these potential concerns, but you’re really hoping you never have to use this. So you’re paying premium for an insurance product. Well, the health screening allows the member to get money back and we default to $50, and that’s each member on the plan. So that’s the employee, the spouse, and all the children. If they have a wife and three kids, all five of you can get a health screening benefit back [00:12:30] every year.

Jason Powers:

I mean, I think with something that’s important for someone to realize as they’re sitting down with a group of employees talking about that kind of benefit, all the health plans out there include preventative care at no cost. So going in for their yearly wellness screening, filing the claim under their critical illness, they get a $50 reimbursement for something that didn’t cost them anything under their health plan to start with.

Greg Cain:

Correct. [00:13:00] Yeah. Got it. It’s just a way to, it really, really reduces their overall premium and puts money back in their pocket. And then similar to all three of these products, it is portable, so the employee can take this, so they leave the employer, the policy that they can take it with them with a portability provision

Jason Powers:

And it’s guaranteed issue or proof of good health is not required here. So there’s no medical underwriting.

Greg Cain:

Correct. Yeah. So great question. If they’re timely, [00:13:30] it’s guarantee issued, it works almost exactly like voluntary life. So if they enroll when they’re first eligible guarantee issued, and there’ll be limits to it, the max benefit is usually $50,000. Case size will determine how high that guarantee issue will be, but as long as they come on timely, they can get access to the guarantee issue level. And then the portability is also a guarantee issue. They can take what they have in force with them. If they’re a late entrance, then a statement, health is required.

Jason Powers:

Sure. Just like wildlife. Got it. [00:14:00] Now we move on to another product. Right. Yeah. So accident’s something that I feel like this is new or is this,

Greg Cain:

We’ve been a marketing accident for about three or four years now. Okay.

Jason Powers:

Yeah, just again, Jason doesn’t talk about accident policies a lot, so this is something that we certainly want brokers to take out as they go into Q four and they’re delivering renewals is another one of those benefits that they can add on. [00:14:30] Yeah,

Greg Cain:

I would say in our space, the accident product and the critical illness are the two that sell the most. And again, like I said, about one out of every three cases that we sell will have one of these attached. And a lot of it’s because of our flexibility in the marketplace for participation, we only need two employees enroll to write these products. So the accident product, I mean, like you mentioned, the commercials we see on the radio, it works just like what we see there. Other than I think our product is positioned a little differently in my opinion. It’s much easier to navigate [00:15:00] and receive value and benefit of a back from our plan as opposed to the traditional plan you might see in the marketplace. And what I mean by that is as we have a lump sum benefit philosophy, so that means it’s one claim, it’s one benefit, and then the claim is done.

For example, if I’m in a car accident and I break my leg, there’s a benefit for a broken leg and we’ll pay that full benefit out. And our claim payments are made within usually 48 to [00:15:30] 72 hours. So the member breaks his leg, submits a claim, they have all their money within a week period. With a traditional plan, there’ll be a benefit for the broken leg, but there’ll also be benefits for rehab and maybe x-rays an ER visit, and you can name the list of expense codes. And the point being is that they have to submit those EOBs and those expenses every single time they come up. So that [00:16:00] claim trail might go six months. And our experience and what we see and what we hear from our brokers is that most employees, they don’t have that discipline to continue to submit expenses.

Jason Powers:

Well, I’ve seen those kinds of policies. Is it a scheduled benefit? It’s got specific things that you have to make sure.

Greg Cain:

So if you were to compare our product and our payouts to a, what I’ll call a traditional plan, because the traditional plan that’s been written for 30 years is the latter. It’s not a lump sum benefit. [00:16:30] We don’t hear people having the discipline to expend those claims. And reality is, look, could that plan maybe pay more? It could maybe pay more, but only if they have the discipline to do that because our lump sum benefit is built to incorporate all those expenses that maybe another carrier has to require six months of expenses to deliver. We can just lump it all up in the first payment and we pay it out. Is it possible that if they do the other way, it’s more maybe, but in our way they’re getting a [00:17:00] quality benefit payback within a reasonable amount of time one week usually, and then they have their money and the claim is done. And so it’s really worked well for us. We have a lot of success with this benefit, and employees really seem to appreciate the simplicity of it. Correct.

Jason Powers:

Yeah. Not as much paperwork to file if you’re just getting it in a lump sum instead of trying to figure out, well, I didn’t have that, but I did have this. And reading that schedule and trying to find [00:17:30] all the documentation that they would need to file that claim could be difficult

Greg Cain:

Too. Yeah, I mean, you kind of hit on the bottom part there. It says no guesswork,

Jason Powers:

Less paperwork,

Greg Cain:

Less paperwork. And that’s exactly how we position it, and that’s how we try to communicate to employees and educate them on how it works. And we tend to get really positive feedback on ’em.

Jason Powers:

That’s great.

Greg Cain:

And then these are just some high level examples. I mean, we can certainly share the specific reimbursements, but again, if you were to compare our schedule of benefits to our competition, [00:18:00] it compares very, very favorably for us. Yeah,

Jason Powers:

I think seeing it on a quote, looking at some of the value of those benefits, I think it probably becomes clear for the employee that it’s an affordable and attainable coverage. And those may not be as scary as say critical illness, but those are all situations that could be disruptive in everyday life.

Greg Cain:

Right? I mean, if you have kids that are under the age of 16, the likelihood [00:18:30] of a concussion is high, and so it’s a $500 benefit and that pays for probably three years with a premium or close to it. So it’s really been a bit of it. That’s complimented our suite of products very well, and it really compliments what most brokers and agents try to do for their

Jason Powers:

Clients. And it’s a little further back in our presentation here. We talked about the chart. We had the chart of the different sizes, but this can be written [00:19:00] down to yes,

Greg Cain:

Same case size requirements, five employees eligible, two enrolled,

Jason Powers:

Two enrolled, voluntary.

Greg Cain:

And I’ll tell you, each three of these products require, we like to see at least 10% participation, and that’s kind of the underwriting guideline. But in our world, we’re writing cases that have multiple lines of coverage, three or more usually. And we’re in that environment, we’re going to waive the 10%, we’re going to go to two lives, and we’re going to make it easy for the agent and easy for the employer to offer [00:19:30] that product on good faith and get something done for them and their employees.

Jason Powers:

That’s great. Yep.

Greg Cain:

The accident product also includes an embedded A and d accidental death and dismemberment rider. So it’s going to be $25,000 for the employee, 12, five for the spouse, an additional 6,250 for the child.

Jason Powers:

This is separate from say the core life and ad and D product. This is a separate benefit attached to the accident plan,

Greg Cain:

Correct? Yeah, exactly right. As we saw earlier, I, and [00:20:00] you’ll probably see another slide here in a second, very similar story here. Coverage for employees, spouse, and kids. Now there is, I will tell you with the accident product, there was a price point for the child election, but we’ve seen these, in fact, our pricing just recently came down to really competitive levels. Quite honestly, for all through all three tiers, it includes a wellness exam benefit as well. Default at $50. There’s some flexibility there. Again,

Jason Powers:

Is it stackable with critical wellness

Greg Cain:

[00:20:30] And the same exact wellness exam? We’ll pay for both. Okay. So you can go to your doctor and have your one physical per year have that one physical be applicable for both accident and critical illness and will pay both benefits out for employee, spouse,

Jason Powers:

And the kids. Wow.

Greg Cain:

Yeah, it really, it is a nice feature. And again, also portable. So yeah, just a really nice solution for us.

Jason Powers:

I did not know that. Yeah. [00:21:00] This is why I like having you here, Greg. Every time you come here, I find something new. You probably tell me the same thing every time and just,

Greg Cain:

Well, these are new, so, oh,

Jason Powers:

I got it. Alright, good. I don’t feel so bad. This is new.

Greg Cain:

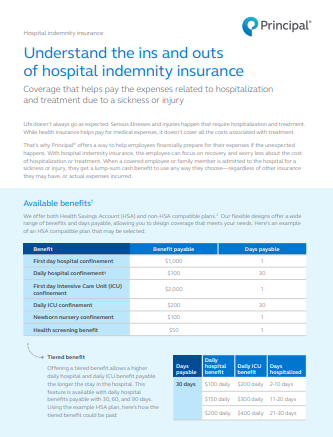

This is not here. Last year, this brand new, within the last six months, yes. Just rolled out. We, this is one where we are still doing some filing and approvals in some states. Most states are approved by now, I couldn’t tell you [00:21:30] the ones that are kind of left over, but here in the Midwest, this is filing approved. We’re right, these coverages, Kansas, Missouri, Colorado, Iowa, things like that. In hospital indemnity, it’s a product that’s built for hospital confinement. So if you or your kids are confined to a hospital, it’s going to pay a benefit for that. And then there’s prolonged stay, then there’s a daily benefit for the continued hospital stay. And again, it’s really built for, we go back [00:22:00] to that major medical event. So name what that is, whether it’s as simple as Covid and they’re in the hospital, or if it’s a heart attack or a stroke or whatever, that first day hospital confinement, a lump sum minimum is going to be paid out.

If it’s prolonged over a number of days, we’re going to be paying a daily hospital benefit for that as well. And then there’s also, as you can see here, that there’s additional payout, a higher level benefit, but if it’s something serious intensive care, there’s also a newborn [00:22:30] nursery confinement. So again, you have a new mom with a new baby, we’re going to pay a hundred dollars for that. There is some flexibility with what these numbers can be. This is the one product, and I didn’t mention this before, but these are all fairly rigid products. I might call ’em shelf products. They’re not shelf rated. What everything principal does is fairly consistent in regards to the pricing of the plans. We do underwrite and price every plan [00:23:00] within its own accord of the census and the demographic of the case. But the benefits are fairly rigid with a few exceptions. I mentioned the wellness exam can fluctuate a little bit. Hospital indemnity, we can increase these payable benefits up a little bit. There’s a little flexibility here, but this right here is a snapshot of really what the product looks like

Jason Powers:

And it’s H SS a compatible. When we’ve seen a resurgence of H S A plans on the health side for years, the pricing differential just [00:23:30] wasn’t there. And then now we see a lot more employers starting to gravitate to an H S A offering. So this could be a gap filler there as well.

Greg Cain:

Everything we do is H S A compatible period. Now, I’ll tell you, if you want to ask us for other options, and it’s in the realm of non H S A plans, we do have some plans that are non H S A compatible. We don’t market them much. We are not the medical carrier. We don’t know what’s going on the [00:24:00] health insurance side, or we don’t know what’s going to happen going forward. So if we write a non H Ss a plan today, and then two years from now the agent moves that plan, that’s a problem. So we’ll always default to H SS a compliant and it really makes the world easy for the agent and client and the employer because they don’t realize worry about what might happen next.

Jason Powers:

Sure. And did I see, well, it’s right there. Again, health screening, the

Greg Cain:

Yearly

Jason Powers:

Wellness, it’s in there. Again,

Greg Cain:

A common slide again, coverage for employees and families. You’ve got [00:24:30] your health screen screening. Again, it’s just the singular event can pay for all three of these products. Wellness exams, which is really nice and a little unique in the industry in my opinion. And then also port a portable. So again, these are all three products that really in the industry were built on the individual side of the house. There are some good carriers out there that do individual insurance that have, we mentioned commercials out before that carriers, they’ve been around for a long time. They’ve been writing these products for a long time. They’re built on employee ownership [00:25:00] and employee really true portability. They’re individual products. These are all group contracts, group price benefits, but with the ability for the employee to take these coverage with ’em if they want ’em, which is nice

Jason Powers:

Again and again, guaranteed issue. No, as long as it’s timely enrollment, guaranteed issue and all those benefits are stackable.

Greg Cain:

Yeah, exactly right.

Jason Powers:

If I do the math with a family of six at $50 a pop [00:25:30] for a wellness exam, knowing that everybody’s going in for their annual checkup, that that’s $300 a year per line of coverage. Correct. So if you get critical illness, accident and hospital indemnity, I can’t do the math that fast. Was that 900 bucks a year? Yeah. I can’t imagine the premium being much higher than that.

Greg Cain:

Probably not. Yeah. Yeah.

Jason Powers:

So I can’t say free, right? It’s not free coverage, but potentially the offset and premium [00:26:00] would be, or the premium could be offset by the benefit just under the wellness plan very

Greg Cain:

Quickly. Yes,

Jason Powers:

Exactly.

Greg Cain:

Okay.

Jason Powers:

Yeah. Why didn’t I sell these things when I was a broker? I don’t know.

Greg Cain:

I’m not sure.

Jason Powers:

Well, you should be selling ’em. So do yourself a favor. Make sure that you’re looking at principle for your supplemental needs, not just your core dental, vision, life, disability, but look at principle for critical illness, accident and hospital indemnity. [00:26:30] Right? Yeah.

Greg Cain:

Yeah. Thanks for having me. I appreciate it.

Jason Powers:

Any parting words for brokers as they embark in the craziness that’s already upon us? Well, it’s

Greg Cain:

Fourth quarter. Go sell something, fourth, go sell something. We all got to do that. Right? It’s go time.

Jason Powers:

That’s right. That’s right. Well, if we can help you with your principal quotes or any questions you have on the proposals you have, be sure to reach out to our staff here at Legacy Brokers. Greg, once again, it’s always a pleasure having you in. Yeah, thank you. Appreciate [00:27:00] you being here.

Greg Cain:

Yeah, appreciate it. Thank you.

Jason Powers:

Happy selling.

Jason Powers:

Thank you for watching this edition of our carrier product update series. Visit our website to watch other episodes.

Frequently Asked Questions

Who is Legacy Brokers?

We are a General Agency that focuses on group health and ancillary insurance products. We are the experts in small group self-funded and fully-insured products. Our clients are licensed insurance agents, just like you. It doesn’t matter if you focus on P&C, Financial Services, Medicare, Life and Annuities. If you have a health insurance license then we can help you win more business.

What services does Legacy Brokers provide?

- We run your quotes

- We help you analyze the quotes

- We assist you with the sale

- We help you service the case

- We help you renew the case

Does using Legacy Brokers cost me anything?

We have a GA contract with many of the carriers that we quote. For those carriers, we earn an override and you earn 100% of the producer commissions, so it will cost you nothing! With that said, other carriers may be a little different and the commission structure could vary from case-to-case. Whatever the circumstance might be, our number #1 goal is to help you maximize your profits for each case every year!

How do I get started?

That’s the easy part! We can start the process in a number of different ways.

- Click on the blue “Speak to an expert” button at the top or bottom of this page, fill out the required information and an expert will get back with you in less than 24 hours.

- Call or email us directly: 1-800-844-1901 or 913-631-0102 / sales@legacybrokerskc.com

Who owns the Client?

You Do! Whether we operate side-by-side or one step behind you, we never jump in front of you because it’s YOUR client. It’s our job to continuously earn your trust and service your business throughout the year. If you ever wish to move your business, you are free to do so with your clients in tact at any time – with no strings attached. Our goal is to be YOUR trusted advisor along the way.

Get your marketing materials for Principal right here.

Send us your Principal quote request now!

Agents - Are you looking to get a quote for a group?

Carrier you may also like

UnitedHealthcare

UnitedHealthcare offers benefit solutions for groups as small as 2 employees using the largest proprietary provider network in the United States. Their self-funded option, All Savers, gives 2/3 of any claims surplus back to the group. Plus, they offer competitive ancillary options like dental, vision, life and disability coverage.