Carrier – Aetna

Agents - Are you looking to get a quote for a group?

Aetna is one of the nation’s leaders in health care, dental, group life, disability, and employee benefits. Aetna’s diverse product portfolio offers benefits and services to help meet the needs of individual families, small, mid-sized, and large multi-site businesses.

Interested in other Carrier Product Update Videos? See all videos here.

03:06 — KC Care Network Plus Overview

05:13 — Moving from Essential to Standard Plans

07:28 — Over the Counter Health Solutions

09:45 — Diabetes care offerings

15:24 — 51-100 Dual Quoting & National Portfolio Launch (Fully & Self Insured Quotes)

16:48 — 51-100 Fully Insured and AFA (Commission vs PEPM)

18:39 — Underwriting Guideline Changes

19:05 — Savings now, surplus later

22:22 — Aetna Funding Advantage – Savings when you Bundle Ancillary

Jason Powers:

It is time for another carrier product update. Tune in as we talk directly to the carriers about their new plans, any new network options they have, or which plan designs offer the most savings and learn about the tools and resources they offer to help you generate more business. Visit our website to learn about all of the carriers we quote in our carrier product update series.

Hello and welcome back to our carrier product update series. This is our Q four kickoff summit. [00:00:30] I’m Jason Powers and joined by a very good friend of mine, Kim Williams of Aetna. Welcome to the Welcome to This is your first time.

Kim Williams:

This is my first time, Jason. Oh,

Jason Powers:

I’m so excited.

Kim Williams:

Thank you so much for having me today.

Jason Powers:

I don’t want to make Darryl feel bad, but I’m glad Daryl couldn’t be here today.

Kim Williams:

Yes, Darryl’s traveling, so I’m the lucky one.

Jason Powers:

Love it. Well, Aetna’s a wonderful partner of ours. We are a general agent contracted with Aetna. So everything that we do [00:01:00] with agents out in the market, our services don’t cost you or your client anything additional in the premium Aetna’s contract with us is to pay us our general agent override and you receive a hundred percent of the producer and production credit. So it’s a great partnership. For those that aren’t familiar with Aetna, which I think would be tough to say in a market like this, but for an agent that may not be familiar with Aetna, what can you kind of sum up as sort [00:01:30] of Aetna’s Aetna’s position in the market?

Kim Williams:

Well, we’re very strong in the marketplace. Aetna was actually the first carrier to come up with the level funded product for small group. We’ve been very successful at it and we have a lot of value added benefits to our plans.

Jason Powers:

I remember when the, A product was kind of hitting the test market segment way back,

Kim Williams:

Right about the Affordable Care [00:02:00] Act

Jason Powers:

Roll way back, and

Kim Williams:

We had to look for another way to offer cost-effective benefits.

Jason Powers:

Yeah, it it’s interesting to see the graduation of the product and the more sophistication of the product over time. You certainly have as a company, I think have listened to market feedback, listened to member experience, and built a product that I think stands really tall [00:02:30] in the market and agents that are maybe not giving Aetna a look probably ought to rethink what they’re doing. Absolutely. And their strategy need to rethink, rethink and consider it for their small group cases. For sure.

Kim Williams:

Absolutely.

Jason Powers:

So let’s get into what’s new because we’ve got some exciting stuff to share I think that agents haven’t heard yet. I think there’s maybe some breaking news coming here soon, here soon, right here and [00:03:00] this, you’re going to hear it first right here? Yes, you will. All right. Let’s jump into it.

Kim Williams:

As many of you know, we have the I 35 network used to be called the I 35 Network, and these are predominantly hospitals that followed the I 35 corridor. Well, we’ve increased that network significantly, and so we’ve renamed the I 35 network, the KC Care Network, plus there’s a map up here that shows [00:03:30] the different areas that we have providers in this network. We have every single hospital in the greater Kansas City area, with the exception of St. Luke’s. So this is a very good network to use as a base network. You do have to reside within certain counties to be able to enroll in this network, but we’re very excited about the addition of the hospitals and expanding that footprint,

Jason Powers:

And [00:04:00] I think this is a great name change. I think the I 35 name was, I think it described right, described that

Kim Williams:

I 35 corridor where we had the hospitals, but as we expanded.

Jason Powers:

Yeah, yeah. I think as you expand, you have other hospitals that maybe aren’t on I 35. It helps kind of paint the picture of this is a case, Kansas City specific network. This can be paired with the larger choice POS two product that can be [00:04:30] offered to anybody outside those service area, but certainly is a great cost saving alternative.

Kim Williams:

It’s also important to note, Jason, that members have reciprocity to our open, our National CPAs network as well. So if they’re traveling or they’re needing care in another state, they’ll be able to access that. They’re not just limited to this specific network,

Jason Powers:

It’s just in Kansas City. If they’re in those service areas looking for [00:05:00] providers, they need to stay in that network. Outside of that, you get the wrap of the national product. That’s great. Love it. Love it. I love the name Change too. KC Care.

Kim Williams:

So we had some plans that were called Essentials or the Open Access Select, which were really e p O plans. They didn’t have an out-of-network benefit. We weren’t getting much mileage with those plans just because there wasn’t enough cost savings [00:05:30] between the essentials in our standard CPAs plans. So as you can see, we’re going to be moving away from essentials and we’re going to migrate those popular essential plans over to our standard plans, so they will see those effective nine one on a new portfolio.

Jason Powers:

Got it. Those standard plans existed before. These aren’t new plans, correct? They’re just mapping members from the essentials over to the standard product? Yeah,

Kim Williams:

That’s correct. Except for that last one, that 9,100. [00:06:00] So that is a value plan. So our value plans look and operate very much like an H S A plan, but they’re not H SS A qualified, so they’re going to be actually our lower cost plans. But again, don’t qualify as an H

Jason Powers:

S A just because they’re higher deductibles and higher out-of-pockets.

Kim Williams:

Correct.

Jason Powers:

Got

Kim Williams:

It. So that would be the one new one. Yep, yep. Premier Plans, we are adding these [00:06:30] to our portfolio ten one, as you know, a lot of the grandfathered plans are moving, particularly grandfathered Blue Cross Blue Shield plans and moving away from a c a, and so Aetna’s looking for a way to closely match those plans so they have something to move to that’s similar. The premier plans are going to be richer in benefit. You could see that they do have a $20 copay for primary care [00:07:00] and 40 for specialist, and then zero on lab and x-ray. So again, lower cost sharing to our members on these plans.

Jason Powers:

And there’s eight of these that are added to the portfolio effective Tim one, and really That’s correct. That’s something for everybody to know. These are all of these changes. Aetna does a product refresh

Kim Williams:

In every nine one in

Jason Powers:

September, but these are plans that will be available [00:07:30] effective ten one effective dates,

Kim Williams:

Ten one, and you’ll see those on your proposals coming out.

Jason Powers:

Got it. I love this one. Nice.

Kim Williams:

This is one I’m really excited about. So ten one, we’re rolling out the over the counter health solution. So each one of our members will be given a $25 allowance each quarter, and they can use that for any C V S brand products. So it’s predominantly anything that’s F SS a qualified, so coughs [00:08:00] or Band-aids, ibuprofen, anything of that nature, that C V S brand, they will get $25 allowance per member. So you can see if you have a family of four, it’s $400 a year. Now that $25 doesn’t carry over each quarter, so you have to make sure that you use it because if you don’t, you lose it. No rollover.

Jason Powers:

Got it.

Kim Williams:

They have several ways. I think on our next slide, it will show there’s several ways that they can access, no, I’m sorry. There’s several ways [00:08:30] that they can access this benefit. So they can go into the store and show their member ID card at the checkout. The cashier will put in their member ID number and apply that allowance at the time of sale. They can also go online to cbs.com and they can order online and they can also order over the phone. The one thing is they’re not in the store. They have to meet that exact $25 or be a little bit [00:09:00] under it because we don’t have a way for them to pay an additional cost over the allowance. Sure. If they’re in the store, then they can Sure makes sense. But no, very excited about this benefit. I think it’s huge.

Jason Powers:

Yeah, we’ve, because this rolled out for nine one with the product refresh, we’ve already seen some nine one cases that have been installed, nine one renewals that have renewed, and agents, I’ll tell you, the feedback that we’re getting from the agents in the market and the members that they’re talking to is really positive. [00:09:30] I think this does a really good job of tying in the C V s brand and c V s ecosystem, if you will, to the healthcare delivery model that is Aetna. So it helps round things out and we’re excited about it.

Kim Williams:

Agreed. This is another benefit that I’m excited about too. Diabetic care offering. So for our members that are insulin dependent, we will cover insulin at a hundred percent. So [00:10:00] zero cost to our members. It does have to be an insulin, Jason that is on the drug list as either a generic or a preferred name brand. So when you go out and look at our drug formulary, any insulins that fall into those categories, tier one, tier two, are going to be at a zero cost to our member. We’re also covering all of their diabetic supplies at no cost. So their strips, their monitors, the lancets, all of that will also be covered at a hundred percent.

Jason Powers:

[00:10:30] And I think this speaks to the commitment to members. These are what we don’t want to do in the healthcare space is put a barrier between someone who is dependent upon insulin to live. Absolutely. And I think it’s a really responsible response from Aetna and member feedback to build a benefit that I think is valuable to those that are [00:11:00] seeing over the last few years, more barriers to getting their insulin. And it’s the last thing that any agent needs is a phone call from a member who can’t get their insulin. It’s different than from a member who can’t get their blood pressure medicine. Not that that’s not as important, but I think insulin is one that’s really critical to survival for a lot of

Kim Williams:

Folks. So contributes to a number of other medical conditions that,

Jason Powers:

And it helps keep those members that are diabetic compliant with their [00:11:30] treatment plan. So love it. Love this benefit.

Kim Williams:

This is on our virtual primary care. So as you know, c v S now owns Aetna, and part of that is offering primary care physicians to our members. So C V S has a group of physicians actually owned by C V S. Then our members can now access at no cost. So they can go online and [00:12:00] make an appointment with a physician through cvs.com. It takes about three to five days to get an appointment, which is a lot quicker than if you’re trying to get in with your primary care. We’re seeing a real shortage in primary care doctors now, and for a lot of people, it could be up to two months to get in to see their primary care doctor. So by offering the virtual care to our members, it allows them quicker access to a physician, [00:12:30] also to nurse practitioners and other healthcare providers. So again, all they need to do is go online and make their appointment.

Jason Powers:

I think it’s important to park here for a second and differentiate this from Teladoc or telemedicine, tele aoc, telemedicine benefits, telehealth. Over the last few years, we’ve seen a huge increase in utilization in telemedicine benefits because of covid, [00:13:00] but it was, telemedicine is generally for acute medical conditions. I woke up, I don’t feel good. I need to see a doctor. Telehealth is there, correct. This is adding another level, another layer of care with virtual primary care. So we’ve always said, I think we’ve always said in the market, telehealth is not a replacement for primary care. C v s and Aetna have partnered those [00:13:30] two ideas together to say, well, now we have virtual primary care. So this is maybe not a replacement for,

Kim Williams:

I think it’s an enhancement. An enhancement.

Jason Powers:

It’s additional layer of care that that can be delivered to someone who doesn’t have a primary care physician relationship. Now, they can access

Kim Williams:

One person or somebody that has maybe transportation issues. They want to keep the relationship with their physician, but they maybe need, there are times when they need a [00:14:00] primary care doctor, but they can’t leave their house. You got it. So this is just a supplement. It’s not replacing their relationship that they have with their doctor. And you’re right, there are many ways that our members can access healthcare now. They can through Teladoc, which is still available. It’s an outside vendor that Aetna uses. They don’t have the consistency of the same provider with Teladoc. Whereas this they do with virtual care. With virtual care, they can request the same physician over and over again.

Jason Powers:

Right. I [00:14:30] talked to this doctor last week about this situation. I need to give them an update and talk to ’em about what’s going on now. So it does kind of change that dynamic. I think, again, I just feel like it adds another layer. Kudos to Aetna for developing that with C V S and delivering that for our members.

Kim Williams:

And we still have MinuteClinic MinuteClinics a real great resource too. You can just walk into any C V s MinuteClinic and access

Jason Powers:

Care. And in the portfolio, is it all [00:15:00] plans except for the H S A that have that at no cost? That is correct. Yeah. So that is C V s MinuteClinic being able to walk in or schedule an appointment. You can go online schedule appointments with the C V S MinuteClinics at zero cost on all plans except for H S A, which have some small,

Kim Williams:

It’s a minimal cost,

Jason Powers:

Small cost associated with it. You have to in order to be H SS A compliant.

Kim Williams:

You got

Jason Powers:

It. Great.

Kim Williams:

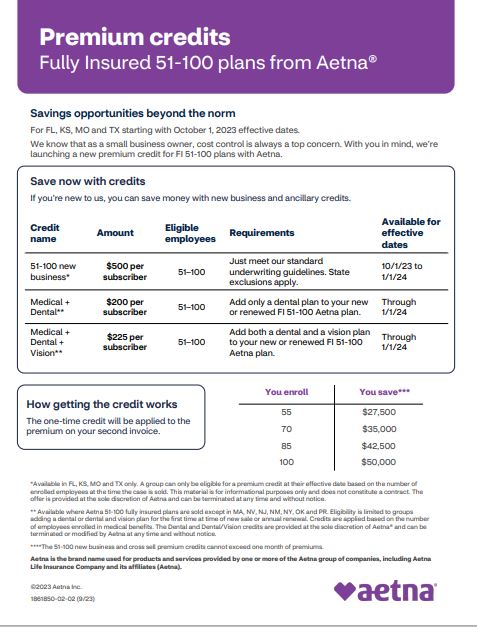

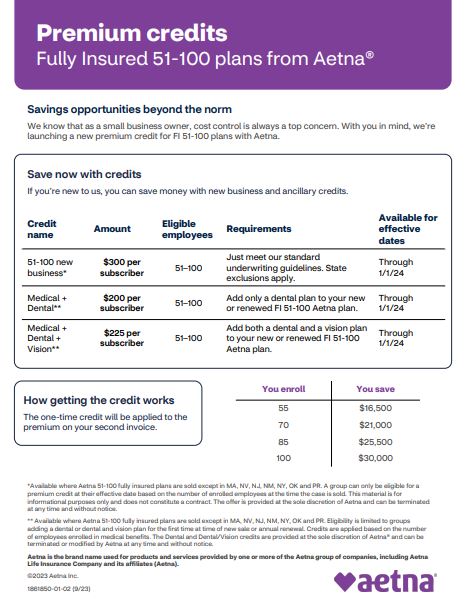

So on our 51 to 100, we’re now able to quote both a F A and [00:15:30] level funded. So when you get a proposal, you will see that we have both options quoted. This is actually a pilot project that Aetna is doing in the states of Florida, Kansas, Missouri, and Texas. So we started, we rolled this out, 7 1 4, 10, 1 effective dates. And I love the fact that you get one proposal and it’s got both options. Jason, you’ll only see about a 1% decrement in cost when you’re [00:16:00] looking at the a FFA versus the fully insured. So there’s not a huge cost savings to do fully insured.

Jason Powers:

But I think for the agents that are trying to move a group off of fully insured and start thinking outside the box a little bit with level funding to be able to show them side by side, and they’re both Aetna banners instead of here’s a fully insured option from another carrier versus Aetna’s level funded, it makes that conversation a little bit easier. [00:16:30] So again, really excited about this.

Kim Williams:

Yeah, we’re able to do that now and we will talk a little bit further about the admin credits, but admin credits will apply to both

Jason Powers:

On this. I know. I’m excited about what’s coming.

Kim Williams:

This just kind of discusses the commission levels. So these are standard defaults. In Kansas, it’s $30 P E P M. In Missouri, it’s [00:17:00] 31, Texas and Florida. It’s different. But our brokers can request any level of commission that they desire. And we have moved to A P E P M across the board. It used to be a commission on fully insured P P M on a f a, but going forward, it will just be P P M.

Jason Powers:

Yeah. We had a conversation with a broker the other day that was talking about the difference in percentages versus ppms, and it helps [00:17:30] them with their communication to clients that, look, their commission isn’t driven by premium, so it’s not when they get a 10% increase in premium, the broker’s not getting a 10% increase in pay. They’re still offering the same services at the same cost. It’s really the cost of insurance that would be changing because the cost of care is changing, although it just helps lead into that conversation, goes right into the claims reporting,

Kim Williams:

And it makes us fluid across both

Jason Powers:

Platforms. And I think it’s becoming more standard across the industry. There’s still some products out [00:18:00] there that do percentages of, but I think that P P M really helps change the conversation for brokers that are migrating to that consultant level delivery model.

Kim Williams:

You’ll also notice there off to the right, it does make mention that we still offer the value added plans, the C V S integration, MinuteClinic virtual care, and over the counter

Jason Powers:

And excluded in Missouri on the O T C benefit for 51 and 99 fully insured in a ffa.

Kim Williams:

Yes, [00:18:30] that’s a Missouri, just

Jason Powers:

A Missouri mandate only mandate. And only in that space. It still applies in the small group space O TC credits.

Kim Williams:

Just some of our underwriting guidelines. We are now allowing retirees on a f a, which we hadn’t. Yeah, it’s new. Yeah, we hadn’t in the past. So as long as we don’t have over 10% of the total population we’re good. And then again, we mentioned the commissions will go [00:19:00] to P E P M.

Jason Powers:

Here we

Kim Williams:

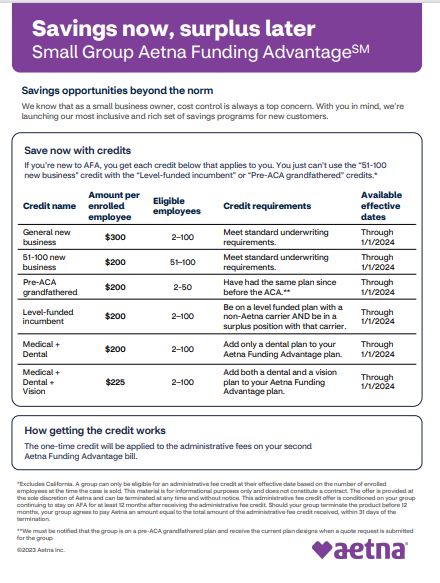

Go. I love this. This is our savings now and surplus later. So we’ve gotten a lot of mileage off of these credits

Jason Powers:

And up until today, yes, this was going through and 1215 effective dates. That’s correct. But you’re here to announce that

Kim Williams:

As of today, we will run this through January. So this credit will also be available for January one business. Yes. [00:19:30] So just a quick glance at how this works. So when you write a new group with us, general new business is going to be a $300 per subscriber. So while however many you have enrolled, it’s $300 per head. If you have a group that is pre a c a, they’re coming off a grandfather plan, we’re going to give them an additional $200. So now you’re at $500 per sub. If they are a new business [00:20:00] and they’re fully insured now, or I’m sorry, level funded now, and they’re in a surplus position, then we’ll give them an additional 200.

Jason Powers:

Why would that be important? Because certain products, like certain products do have a provision that says you have to renew in order to get that surplus. So you may have a case where that renewal is a little higher than what the client is willing to accept, but they really don’t want to walk away from their surplus. What Aetna is saying here is, Hey, we’ll [00:20:30] give you an extra $200 admin fee credit on top of the other. These are all stackable. Exactly. So on top of the other credits that they apply for, you’ll get an extra 200 because you’re in a surplus position and

Kim Williams:

It just helps offset that loss of the surplus from

Jason Powers:

The other carrier. And again, although the screen here says available through 12 one effective dates, this has now been approved through January 1st, 2024 effective dates. Correct. So keep that in mind. You got some ideas on the [00:21:00] side here for about surplus. That’s in addition to admin fee credits, right?

Kim Williams:

Yes, it is. So after our 12 contract, we look at the group and we take the premium that they’ve paid minus the claims that Aetna’s played, and if there’s money left over, that’s a surplus and the group would get 50% of that surplus back if they renew with us. So what we’re saying here is if you’ve got a group of 15, we’re going to guarantee $20,000 [00:21:30] surplus regardless. Wow. 2000. 2000. If the group’s running well and it’s over that amount, they’ll get the higher amount, but we’re just guaranteeing that they’re going to get something

Jason Powers:

Back. So even if they have some surprises, have a terrible claims year and far exceed their loss ratio, they’re guaranteed to get something back by enrolling in the a FFA product? Correct. But again, they do have to renew in order [00:22:00] to get the surplus returned. And the surplus reconciliation happens about

Kim Williams:

45 days. 45 days,

Jason Powers:

45 days after the contract ends. And it’s a deposited back into the same

Kim Williams:

Account? It’s back into their bank

Jason Powers:

Account. Yeah. It’s not a credit. So it’s a deposit back into the bank account, and

Kim Williams:

The employer can do whatever they want with that. Got it. There’s no restrictions. So also we have admin credits for dental and vision. We’re writing a lot of dental and vision. [00:22:30] The dental is with Aetna Aetna’s dental plans, and then vision is through immed. So if you add dental to the medical, there’s an additional $200 credit. And that is based upon the medical subscribers, not the dental subscribers. So depending on how many you had enroll in medical is going to be what we pay in credit for dental. So two,

Jason Powers:

And again, the stacks on top of the previous screen where if it’s a [00:23:00] $300 for new business and they add dental, now they get to 500. If they add dental and vision, that goes to 5 25. So it’s stackable. Plus if you have a group that has surplus position with another carrier that they’re moving off of, and I know we’re probably going to talk a little bit about the Humana exit, but specifically there may be Humana cases that are in a spot where they want to get moved off of that Aetna contract into an Aetna contract. This gives them [00:23:30] the ability to walk away from any surplus position and stack these credits

Kim Williams:

Together. So for example, if you’ve got a new group, it’s a FFA surplus, and you add dental and vision, you’re at 7 25

Jason Powers:

Per subscriber. Per subscriber as a one-time credit on their bill. They may not pay admin fees for the first couple of months.

Kim Williams:

Exactly.

Jason Powers:

Which is fantastic. That’s great. And then that stacks on top of the guaranteed surplus as well. Correct. All good news. [00:24:00] That’s the update. Wow.

Kim Williams:

And also Jason, just to go back with that credit, that’s on fully insured as well.

Jason Powers:

Oh,

Kim Williams:

Wow. Yeah. So if they’re fully insured, they get that credit, they wouldn’t get the surplus, but they’ll look at that credit even through one. One.

Jason Powers:

It shows up on their second invoice, I believe. So after install second invoice comes out, that’s where those credits will apply. Well, that’s fantastic. I know Aetna’s, again, [00:24:30] been a terrific partner for us. We appreciate you coming on and giving us an update As brokers are kind of heading out there, any words of advice before they head out and start selling? I mean, they’re already, I know they’re already beating down our door for January one rates, any words of advice before they head out into the great unknown?

Kim Williams:

No, just be sure to share all of the added value benefits that Aetna has. [00:25:00] And I just wanted to touch briefly on the Humana transition, because Aetna is looking for ways to make that transition easier for our brokers and our employer groups. So we’re offering different contract months for Humana groups so they can do anything from a 12 month up to an 18 month rate guarantee or rate contract.

Jason Powers:

Right. So we got to quote it that way though, right? It’s got to go through the, you

Kim Williams:

Just have to ask, do you want a 14 [00:25:30] month or 15 month or whatever?

Jason Powers:

Yes. So a case that wants to come out of that Humana contract but wants to keep their original, say they’re a March one, but they want to make the change January one, they can keep that March one renewal and just do 12 plus the two makes 14 months. We just have to know that on the front end, and it’s specific to Humana cases, but we have [00:26:00] to know that on the front end so that we’re quoting it with underwriting, coming back with that firm rate that we’ve got the right contract in place. But that’s not it. That’s not, all right. There’s broker incentives attached to Humana incentives. Humana business coming off.

Kim Williams:

There’s broker incentives for just the general Aetna business as well. Absolutely. And those can be stacked, the Humana incentives on top of our regular incentives.

Jason Powers:

Yeah. 60 [00:26:30] per, is it 60 per subscriber per Humana business? Sort of a one-time incentive to move that. But in addition to that, you’re doing deductible and out-of-pocket credits for Humana business moving over

Kim Williams:

And de all of it. We always have given out-of-pocket credit.

Jason Powers:

Is that across the board for a f a? It’s across the board, yes. I learned, see, Daryl, I learned something new from Kim. Actually, I knew that because Daryl told me [00:27:00] that last week. Anything else specific to Humana transition?

Kim Williams:

We’re g r Xing down to 10 to make that process easier. Okay. And then

Jason Powers:

Down to five, specifically specific to Humana?

Kim Williams:

Yes. Five if they’re level funded,

Jason Powers:

Five if they’re level funded. But we’ve got to have the level funded claims reporting.

Kim Williams:

Correct. Okay. Otherwise 10. Okay. Okay. So yeah, trying to make it simpler for the brokers.

Jason Powers:

You heard it here. You heard it here. [00:27:30] Well, Kim, always a pleasure to see you and always great to hear all the new stuff going on at Aetna. Thanks for coming out and sharing with our brokers.

Kim Williams:

Thanks, Jason. I appreciate your time and the time with the brokers as well.

Jason Powers:

Yeah. All right. So if we can help you with your Aetna quotes, be sure to reach out to our team after this video airs. We’ll post it on our website and to our carriers tab, Aetna starts with a, so it’s the first carrier at the top right below. This video [00:28:00] will be a link to downloadable marketing flyers and more content that Kim shared with us today, so that you can share that with your perspective groups and clients. And then down below that is a button to reach out to our team to help you with your Aetna business. Thank you so much for tuning into this carrier product update. I’m Jason Powers and we’ll see you next time.

Thank you for watching this edition of our carrier product update series. Visit our website to watch other episodes.

Frequently Asked Questions

Who is Legacy Brokers?

We are a General Agency that focuses on group health and ancillary insurance products. We are the experts in small group self-funded and fully-insured products. Our clients are licensed insurance agents, just like you. It doesn’t matter if you focus on P&C, Financial Services, Medicare, Life and Annuities. If you have a health insurance license then we can help you win more business.

What services does Legacy Brokers provide?

- We run your quotes

- We help you analyze the quotes

- We assist you with the sale

- We help you service the case

- We help you renew the case

Does using Legacy Brokers cost me anything?

We have a GA contract with many of the carriers that we quote. For those carriers, we earn an override and you earn 100% of the producer commissions, so it will cost you nothing! With that said, other carriers may be a little different and the commission structure could vary from case-to-case. Whatever the circumstance might be, our number #1 goal is to help you maximize your profits for each case every year!

How do I get started?

That’s the easy part! We can start the process in a number of different ways.

- Click on the blue “Speak to an expert” button at the top or bottom of this page, fill out the required information and an expert will get back with you in less than 24 hours.

- Call or email us directly: 1-800-844-1901 or 913-631-0102 / [email protected]

Who owns the Client?

You Do! Whether we operate side-by-side or one step behind you, we never jump in front of you because it’s YOUR client. It’s our job to continuously earn your trust and service your business throughout the year. If you ever wish to move your business, you are free to do so with your clients in tact at any time – with no strings attached. Our goal is to be YOUR trusted advisor along the way.

Get your marketing materials for Aetna right here.

Send us your Aetna request now!

Agents - Are you looking to get a quote for a group?

Carrier you may also like

UnitedHealthcare

UnitedHealthcare offers benefit solutions for groups as small as 2 employees using the largest proprietary provider network in the United States. Their self-funded option, All Savers, gives 2/3 of any claims surplus back to the group. Plus, they offer competitive ancillary options like dental, vision, life and disability coverage.