Carrier – Kansas City Life

Agents - Are you looking to get a quote for a group?

Kansas City Life Insurance Company and its longstanding record of financial strength help you prepare for whatever the future may bring. We’ve made Security Assured a way of life and you can, too. From life insurance to annuities, Kansas City Life offers a full range of solutions to meet all of life’s changing moment.

Interested in other Carrier Product Update Videos? See all videos here.

Jason Powers:

It is time for another carrier product update. Tune in as we talk directly to the carriers about their new plans, any new network options they have, or which plan designs offer the most savings and learn about the tools and resources they offer to help you generate more business. Visit our website to learn about all of the carriers we quote in our carrier product update series.

Hello and welcome back to our carrier product update series. This is a very special edition of our carrier product update [00:00:30] series. It’s our Q four kickoff summit, finishing up Q four in 2023 heading into the January renewal season. My name’s Jason Powers with Legacy Brokers and I’m joined today by Amy, an Gotti Bilbo sales representative from Kansas City Life. First appearance here in the Legacy Studio. Very

Amy Angotti-Bilbo:

Exciting.

Jason Powers:

We are super excited to have you. Thank you for being

Amy Angotti-Bilbo:

Here. Thank you so much for having us.

Jason Powers:

Yeah. We are a general agency for Kansas City Life, so Kansas City Life is contracted with us to pay us an override, [00:01:00] which means that you as the producer get 100% producer credit as well as a hundred percent of the producer commissions and any other bonus incentives. It does not cost you or your client anything additional to have legacy brokers work on your Kansas City Life proposals. So we’re familiar with you as a general agent. You’ve done a great job of getting our staff introduced to the Kansas City Life product portfolio, but we’ve got agents out there who have never probably seen any Kansas City Life proposal. [00:01:30] They may not get in that ancillary space. So two minute elevator pitch. What would you describe as your position as a carrier in the market?

Amy Angotti-Bilbo:

Sure. Well, we like to keep it as simple as possible. We are a small carrier. We always say small enough to compete large enough to care. And our target market is really, we have a product series for two to nine lives and then for I’d say 10 to 500. But that everyday sale being under that a hundred, we love to do multi-lines. So the life L T D, sd, dental Vision, [00:02:00] critical illness and accident. And the key thing with us is that you have very limited points of contact, which is good. So you have obviously you as the ga, myself and then our sales coordinator, and then the group is assigned to one administrator, so one bill. So really one point we kind of wrap ourselves around one point of contact. I think that’s our biggest selling feature in the market is it’s very easy to do business with us because we don’t have a lot of contact, A lot of points. You’re going to myself or that administrator

Jason Powers:

And we certainly appreciate that we don’t get lost in the maze [00:02:30] of pressing one or two. Yes.

Amy Angotti-Bilbo:

Well, and whether you have a group that’s two lives or 300 lives, they’re all treated equally with that one point of contact, which I think that’s pretty big in the market. I know that sometimes service gets lost.

Jason Powers:

That’s great. I know you’ve got presentation to brokers a little bit. They’re a little bit more about KC Life here.

Amy Angotti-Bilbo:

Perfect. So who is Kansas City Life for those of you that don’t know? We actually have been around since 1895, but doing group benefits for over 50 years. And I [00:03:00] always say, like I said earlier, we are small enough to compete large enough to care. We offer Midwest hospitality with excellent customer service, which is key. And again, life L T D, sd, dental, vision, CI and accident, some key things. We are fully integrated with employee navigator. We can also do the 8 34 file feed. So these are just some key things that I’m going to touch base on and then we’ll kind of dig into the products. Sure. The dashboard is our online service model, so where you can make ads, changes, deletes, print your bill, [00:03:30] pay your bill, and we won’t do a tutorial of that now, but we can do a quick tutorial later on if you’re interested in learning more about our online capabilities.

I mentioned the dedicated client service specialist, which is key. Again, the one point of contact. Another thing is, is that we can do the cannabis industry, which not all carriers will do, so we can do all lines of coverage for cannabis. We just have to make sure they’re W two. They’ve been in business a year, they have a business banking [00:04:00] account, so that is They can’t bring cash. They can’t bring cash. No. Yes, we do want a business check and not a personal check. The other thing is obviously multiple year rate guarantees, and I’ll kind of get into this a little bit later. And then one to two write guarantees on dental. So that’s kind of just the generic overview that we just kind of want to touch base on today and just obviously give you a quick and skinny on Kansas City Life and hopefully you’ll want to do more business with us.

Jason Powers:

That’s great. Well let’s get right into your presentation then. Sure.

Amy Angotti-Bilbo:

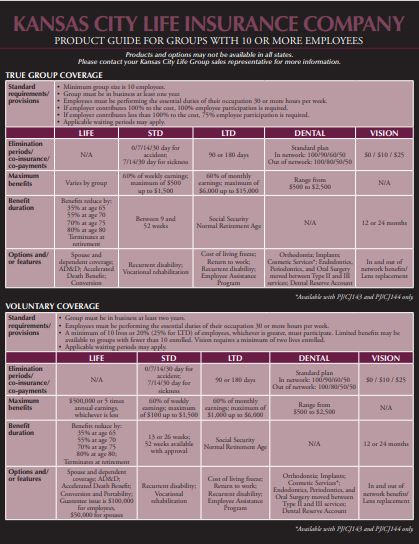

Something that Jason can send you to, this is kind of our cheat sheet. So we have a cheat sheet [00:04:30] for 10 plus, which this is the 10 plus 10 to 500, and then we have a cheat sheet for the two to nine, and I’m not familiar, do you do much? Two to nine? Yeah, a lot of two to nine. So just know that the purple is the 10 plus and then I’m going to have Bob go to the next slide. And then the green is for the go-to and that is the two to nine. So some key things on the go-to. Obviously we offer the life S T D L T D, dental and vision. We can go down to two lives enrolled. It can be offered as employer paid or voluntary, and it’s the same [00:05:00] product as true group, just obviously on a smaller chassis, which we call the go-to.

Jason Powers:

Yeah. And if you’re watching this online, on our website down below, we’ll have links to these product grids so that you can actually see those. Okay.

Amy Angotti-Bilbo:

The other key thing, and I’ll just point out some key features real quick on the life we can go up to 50,000, all guarantee issue there is a dependent life benefit that is attached to that as well. Again, all guarantee issue. The S t D key thing on the S T D is there’s no pre-ex, whether it’s [00:05:30] voluntary or employer paid. So a group of two to nine could come on without pre-ex, you can go up to $1,500 benefit, obviously a 13 or 26 week benefit duration. So great plan designs for small groups, the L T D has a little bit more restrictive of a pre-ex. It has a 12 6 24, but again it’s 60% to 5,000 or at the top three salaries qualify, we can go up to a 7,500 max. And again, on a small group, these are great plans. The dental, [00:06:00] we have five plans that we offer. We can do a Mac, a 90th U C R, we can go down to two for orthodontia. So again, it’s priced appropriately, but there is a benefit that people can take, employers can take advantage of. And the vision, we go down to two and that can be with V S P or Davis, so they have the option of either, but that’s just kind of a little bit on the go-to. And then I’ll kind of get into what we offer extra when we go to the next slide.

Life and a d [00:06:30] D highlights. So with the wife, s t D and l t D down to two wives, we offer the value added services and that is through generally, generally is in over 200 countries. And kind of what this does is it’s an extra service, so it’s not so much a benefit as it is a service, but the travel assistance, if you are traveling a hundred miles outside of your home and less than 90 days, if you lose your wallet or your license or your glasses of prescription, your meds, obviously we can assist you in a quicker fashion than you hunting [00:07:00] and pecking and trying to find it. The beneficiary companion essentially is if you have a loved one that passes and the estate or the spouse does not want to handle the government documents, social security credit card, the spouse can give us permission to help them cancel and talk to those folks.

And then ID theft assistance basically prevent, detect and resolve. If you do have something that happens to you, which we all do, we can send out packets of information to help you remove yourself [00:07:30] from those lists anyway. So again, it’s just a truly, it’s free, it’s no additional charge. It’s automatically included in the rate, which I know we say nothing is free, but it is, it’s baked into it. It’s included in the rate. Yes, obviously flexible benefit plans, reduction schedules, guarantee issues, 1, 2, 3 times salary, flat amounts on the life. And obviously you can be offered as employer paid or voluntary and on the voluntary kind of some standard plan designs, but increments of 10, up to half a million, we can do a hundred [00:08:00] thousand gi, 150,000 gi. It just kind of has to make sense for what’s, if they have an enforce or the group size. But we do offer a true open enrollment for voluntary life, which is key. So when they do come on, it’s a true open enrollment. And then year after year we have an open enrollment for those that either did not come on or that have come on. So I can pause because I’m talking kind of fast.

Jason Powers:

So yeah, I want to back up on that. So on voluntary life, we can do a true open enrollment each year, each year, not just an incremental.

Amy Angotti-Bilbo:

Sure. So what happens is, so obviously the group comes on as a new group is [00:08:30] effective with us, so we treat that as new where everyone can come on whether they had it before or not from the previous plan, and they can come on up to the GI without evidence. And then let’s say year two you had some employees waive year one they can come on for 10,000. And then employees that were enrolled year one, year two, they can increase by 10,000, no evidence of insurability. Now spouses, employees obviously would need to create or would need to complete the E O I, but the employee does not. [00:09:00] So year two and three, it’s I would say a modified, yeah, modified open enrollment.

Jason Powers:

Great. That’s good

Amy Angotti-Bilbo:

Disability. So short and long-term, I always say we can compete with the big boys all day long. They’re just maybe a few differences. But on short-term disability as far as the customized plan designs, we can go up to 2000 max, obviously again, voluntary or employer paid core buy-up, pretty much you name it, we can do it again, flexible maxes is all guarantee issue. Full [00:09:30] scope is who we use for our reinsure and who helps us adjudicate claims, their claim filing. We can do online, obviously email, we are working to have telephonic claim filing. We do not have that yet, but I’m hopeful by next year we have telephonic claim filing, pretty quick turnaround time. It’s a two day acknowledgement, nine day decision for short-term disability, which short-term claims or short-term. So it’s not take too long, but pretty quick. And we have worked with full scope for probably well over 18 years.

So I have obviously clients [00:10:00] and brokers are not calling me when good things are happening. They’re only calling you when it’s an emergency or a claim hasn’t gotten paid. I will say since I have been with Kansas City Life for quite some time, and we do have direct access to those claims managers to where we can get answers to you. If there is an issue that comes up on the L T D very liberal contract, no mandatory rehab, we can do an 80 80 up to a 15,000 max flexible pre-ex an and or definition unlimited return to work. So the [00:10:30] only thing we cannot do on L T D is specialty ooc. So maybe the lawyers or doctors that have the specialty OOC contracts, those maybe are not in our wheelhouse, not that we can’t quote them, but we’re not going to be able to match that specialty ooc.

Jason Powers:

So I’m not a disability guy admittedly. So when you say an and or

Amy Angotti-Bilbo:

So and means loss of duties and loss of earnings and an OR would be loss of duties or loss of earnings? Earnings. Got it. Yes. And there’s a little bit of a load for or, but not much. And I’d say in today’s market we’re seeing a lot more or definitions. [00:11:00] And obviously when you’re quoting, the more information that you send to us, the better. So if you have certs or policies that can show us the details and intricacies of that contract or certificate, it always helps us so that we can match or try to better that plan design.

Jason Powers:

Got it. And that’s important because that one word is really important in

Amy Angotti-Bilbo:

That contract. Yes, it’s important yes. As to how it’s paid and how they review at claim time,

Jason Powers:

If it’s an And then both conditions have to be satisfied in order for the claim to be eligible.

Amy Angotti-Bilbo:

Correct. [00:11:30] Got it. And obviously we have more detailed information and we’re always happy to do another call. We can always do another call or a virtual to go into more detail about disability too. We’re always around to help with that. Great. With long-term disability claim turnaround time, it’s a little bit more just because it’s a long-term claim, so it’s going to be a heftier potential claim that’s involved, but still two day acknowledgement. And our average decision time is about 29 days, which again is pretty typical. Another great feature with L T D is the Kira, which is the e a P. It’s an [00:12:00] actual five face-to-face visits per household, so per employee, per household. So anyone that’s living in the household has access to that E A P. And so that can be for, obviously you have divorce, depression, anything that they need to have a counseling visit for, it’s there for them to be had. We do have a network of counselors based on the area, so they would need to use an in-network counselor, but Kiro has been around for many years. We’ve had a relationship with them for several years, and so they’ve been great to work with. [00:12:30] But again, that e a P is nice. And if the client doesn’t take the L T D and wants to tack the L T D onto another product, they can for 50 cents per employee per month, which is also

Jason Powers:

The E a P on

Amy Angotti-Bilbo:

The a p onto another product.

Jason Powers:

Yeah, I think we’ve seen that on a life product.

Amy Angotti-Bilbo:

Yes, I’m sure you have. Yep. And again, the short-term and long-term are offered on voluntary or employer paid.

Jason Powers:

Great.

Amy Angotti-Bilbo:

Yes. Okay. Dental and vision, we’re just moving and shaking. Yeah. Okay. Dental and vision, we use [00:13:00] what we call the Kansas City Life Dental Alliance and that network features, ax Connection, dental, zealous, we’ll put our network up against anyone. It’s pretty robust. And we can also do a network 360 report. So we can do some reports that show how we stack up in certain areas against other carriers, which also could help the broker as well as the clients so they can see how competitive we are. With our network. Rapid, we average about a five day claim turnaround when we’re paying the claims, very flexible product. So [00:13:30] flexible Max, we can go up to a 5,000 max. Again, it can be offered employer paid or voluntary high low in an out network, Mac 90th, we do have the dental reserve account and that is the rollover feature.

So we can quote that with takeover rollover or you can quote as virgin coverage. So it just kind of depends on what they have in force. But we do have the preventive rewards options, so we can do an additional cleaning for maternity teeth bleaching. We obviously implants would not be considered a reward, but implants obviously should be covered as [00:14:00] well. We no longer, I just found out last night before I did presentation, we no longer have a vision hearing discount, so that should be checked off the presentation, but hopefully that will be replaced with another carrier soon so that we do have that, but we don’t have that as of last night when I found out anyway. Do you have any questions actually regarding the

Jason Powers:

Dental? No dental. I mean dentals usually pretty straightforward on the rollover piece of it. I’m not sure there’s a condition to got to have at least.

Amy Angotti-Bilbo:

Sure there is. And we have, [00:14:30] we have a handout on that that I can give you so you can share with the brokers.

Jason Powers:

Perfect. Yeah, we’ll have that down

Amy Angotti-Bilbo:

Below. Yes, but they need to have at least two cleanings in a year. And then based on your max, it’s kind of based on how you can rollover. So quick example is if you have a thousand dollars plan, use less than 500, you have your two cleanings, you can click carry over two 50 into year two. Got

Jason Powers:

It,

Amy Angotti-Bilbo:

Got it. With Vision, have the choice of V S P or Davis. You can sell those together. However, if you do, they have to be separate bills. So that’s the one time we would not have same billing. Typically you sell [00:15:00] all lines, one line, two lines, it’s one bill. But for if you decide to do two vision plans, you would have two separate bills. With V S P, we use the Choice Network, but again, I know pretty much all the brokers are familiar with Davis and B S P. So flexible benefits, we can go up to 150 max on vision. Obviously safety glasses can be used as the frames benefit through Davis. So there’s some different caveats to the plans that, again, I’m not going to touch base on everything today, but just knowing that we have it and you can quote it so it’s good. [00:15:30] We also offer accident and critical illness. These were our last two products to bring into the market. Super competitive, somewhat competitive. Obviously we can do it on a takeover basis, but with the accident obviously high, medium and low, it is portable. We can do the wellness benefit, we can go down to five lives for accident. For CI we need 10, but for accident we can go down to five. So that is good when you’re doing, if you have a go-to and you’re wanting to offer that.

And then on the critical illness, we can actually quote that. The key thing [00:16:00] on that is we can quote it is cancer only. So that’s also a key feature.

Jason Powers:

So we

Amy Angotti-Bilbo:

Don’t technically have, a lot of times people will say, or brokers will ask if we have just a standalone cancer benefit. No, but we can quote, the critical illness says cancer only. So there are kind of some workarounds on that.

Jason Powers:

Got it. Fills that void if you

Amy Angotti-Bilbo:

Need it. Yes. And on the critical illness, we can go down to five, but for the critical illness we need at least 10 eligible in order to go down to five. So [00:16:30] that’s that.

Jason Powers:

Got it.

Amy Angotti-Bilbo:

Quote request, very similar to what’s standard in the marketplace. So this is nothing new. The only thing that we request obviously with disability is that we want to make sure we have gender nature, we need to have gender, date of birth, occupation, salary, number of hours worked, and if there’s a class out. So I know some carriers don’t always require occupation or salary, but we still do because we ought code and that helps with the rate and helps us break out the group and look [00:17:00] at the demographics. So anyway, that may be something that’s different with Kansas City Life Broker commission schedule. Okay, but how do you get paid? Yeah.

Jason Powers:

And this is a hundred percent broker commissions to the producer of these?

Amy Angotti-Bilbo:

Yes. This has nothing to do with the ga. So these are our standards. So you’ll see our standard is a level 10 on life short-term disability and 15% on voluntary life. You’ll see go to life is also included in there. And then flat 10 and flat 15, flat 15 on accident and ci. [00:17:30] However, our commissions are flexible. We just need to know upfront at time of quote. So I would say the highest that we can go up to is 20%. Anything over 20 is not healthy for our rate and probably not sellable. So as long as we keep it below 20%, we just need to know what they need.

Jason Powers:

Great.

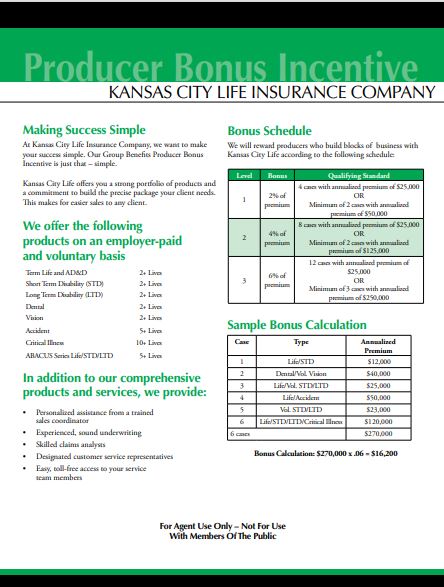

Amy Angotti-Bilbo:

Yes. And producer incentive, how are you going to write extra? Yes, yes. Why are you going to write more with Kinsey Life? Well, because of our producer incentive and there’s still time to hit our bonus, even though we’re going into fourth quarter, you’ll see up here on the chart, [00:18:00] you’ll see level one, 2% of premium. You can write four cases with 25,000 or two cases with 50. So again, 25,000 hits pretty quickly when you’re writing dental. I mean dental it does, we love package multi-line sales. So the more that more lines obviously is better. And obviously this is based off of case or premium, so it’s not how many lines are with or with you. This is a pretty easy bonus to understand and hit. I feel. Level two is 4% of annualized [00:18:30] premium and it’s with eight cases of 25,000 or two cases with 125,000. And then level three is 6%. You get 6% payout on what you wrote in 2023. And that’s any business written one of 2023 through 1231. So as long as you have your 1 1 24 business in-house 1231, you are still getting paid this year on that bonus. And again, it’s 12 cases with 25,000 to hit level three or minimum of three [00:19:00] with two 50.

Jason Powers:

Wow. So we talk about just trying to get to that essentially how big is the bill, how big is the invoice to hit those certain levels? Are there bundling or we talked about trying to package some of those things together. Is there any bundling discounts or package

Amy Angotti-Bilbo:

Discounts? Sure. We definitely do multi-line discounts. And again, if we quote multi-line and there’s four lines quoted and you’re selling too, the rates are going to hold. But yes, we do. And it’s really not a set [00:19:30] percent I would say. I think it depends on what the individual case needs as to what we need to do to get there to write the business.

Jason Powers:

So pretty flexible in that regard.

Amy Angotti-Bilbo:

Yes, very flexible.

Jason Powers:

Good. All good stuff to write more Kansas City Life business, it’s great. And then there’s our local contacts.

Amy Angotti-Bilbo:

Yes, there’s contact. And Vanessa Shaw Potter is who I work with. She’s the group sales coordinator for Missouri and Kansas, and she’s great. She’s been with Kansas City Life over 20 years, so she also like me, the ins and outs of Kansas City Life. So it’s a great team.

Jason Powers:

[00:20:00] Yeah. Great. So again, all the core products, the dental, vision, life, the disability, the voluntary life, the critical illness accident, what’d I miss?

Amy Angotti-Bilbo:

Nothing. One bill. So one bill. One bill, one point of contact. Once the group is implemented, implementation is very smooth. We can do, since I didn’t mention that, but we can do census’s enrollment. We prefer census enrollment versus individual enrollment forms, but we can work with either and the fact that we [00:20:30] are integrated with employee navigators, so that does help too.

Jason Powers:

That’s huge. Yes. So we will have links to the supporting collateral, so some of those product grid information, the different flyers that we’ll talk about, the products that Caan City Life offers. We’ll have that as below this video on our website as well as a call to action to run your Caan City life proposals. Amy, thank you so much for coming in. Thank

Amy Angotti-Bilbo:

You again. Yeah, this was great. Super

Jason Powers:

Fun. Yeah, hopefully [00:21:00] we can build on this and do it again next year and talk a little bit more about how to maybe some strategic things to package some of those products together. We appreciate you being here. Any last words of wisdom for brokers as they head out into what a crazy busy season it is?

Amy Angotti-Bilbo:

Go big or go home. Let’s go. Let’s get some business in the door.

Jason Powers:

Well, thanks again and thank you for tuning in. If we can help you with your Kansas City Life proposals, please reach out to our quoting team. [00:21:30] Operators are standing by. Happy Q four. Happy selling. We’ll see you next time.

Thank you for watching this edition of our carrier product update series. Visit our website to watch other episodes.

Frequently Asked Questions

Who is Legacy Brokers?

We are a General Agency that focuses on group health and ancillary insurance products. We are the experts in small group self-funded and fully-insured products. Our clients are licensed insurance agents, just like you. It doesn’t matter if you focus on P&C, Financial Services, Medicare, Life and Annuities. If you have a health insurance license then we can help you win more business.

What services does Legacy Brokers provide?

- We run your quotes

- We help you analyze the quotes

- We assist you with the sale

- We help you service the case

- We help you renew the case

Does using Legacy Brokers cost me anything?

We have a GA contract with many of the carriers that we quote. For those carriers, we earn an override and you earn 100% of the producer commissions, so it will cost you nothing! With that said, other carriers may be a little different and the commission structure could vary from case-to-case. Whatever the circumstance might be, our number #1 goal is to help you maximize your profits for each case every year!

How do I get started?

That’s the easy part! We can start the process in a number of different ways.

- Click on the blue “Speak to an expert” button at the top or bottom of this page, fill out the required information and an expert will get back with you in less than 24 hours.

- Call or email us directly: 1-800-844-1901 or 913-631-0102 / [email protected]

Who owns the Client?

You Do! Whether we operate side-by-side or one step behind you, we never jump in front of you because it’s YOUR client. It’s our job to continuously earn your trust and service your business throughout the year. If you ever wish to move your business, you are free to do so with your clients in tact at any time – with no strings attached. Our goal is to be YOUR trusted advisor along the way.

Get your marketing materials for Kansas City LIfe right here.

Send us your Kansas City Life quote request now!

Agents - Are you looking to get a quote for a group?

Carrier you may also like

Principal Life Insurance Company

Principal offers a wide variety of ancillary options for employers of all sizes. Check out their competitive dental, vision, life, disability and critical illness plans.